In today’s financial landscape, understanding the true cost of debt is more crucial than ever. As individuals and businesses continue to rely on various forms of borrowing, it becomes imperative to delve deeper into the long-term financial implications that debt can have. This exploration goes beyond the immediate interest rates and monthly payments, seeking to uncover the hidden nuances that can significantly affect one’s financial health over time. In this article, we aim to provide a comprehensive analysis, guiding readers through the complexities of debt accumulation, amortization, and unforeseen economic impacts. By gaining insight into these factors, individuals can make more informed financial decisions and mitigate potential risks associated with incurring debt. Join us as we navigate the intricacies and unveil what truly constitutes the cost of debt across different time horizons.

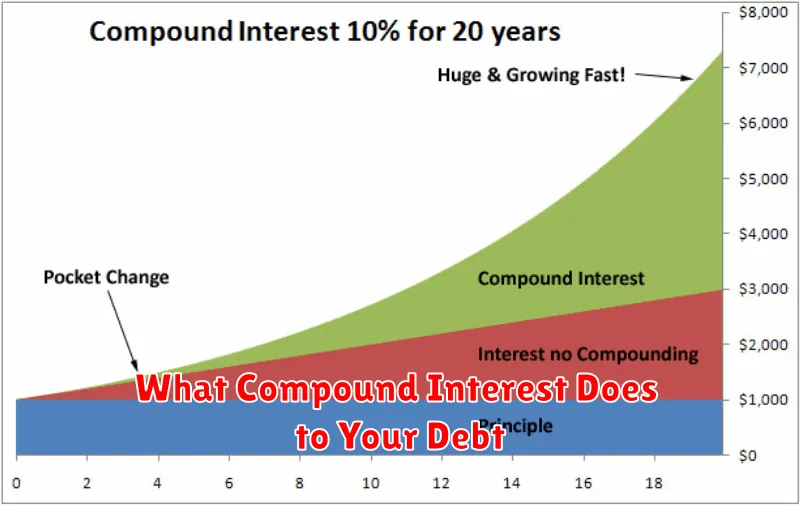

What Compound Interest Does to Your Debt

When discussing finance, one often encounters the term compound interest. While it is frequently celebrated for its benefits in investments, it has a daunting effect when linked to debt. Compound interest essentially means paying interest on top of interest, causing your debt to grow at an accelerated pace.

The fundamental principle of compound interest is that interest is calculated not only on the initial principal but also on the accrued interest. For debt, this means every time a payment is due, the amount is calculated on a higher balance, resulting in a significant increase over time if not managed properly.

This phenomenon can lead to a situation where a seemingly manageable loan can spiral out of control, especially if minimum payments are made. As interest accumulates, the rate of debt growth is faster than the rate of reduction through payments. Therefore, understanding and managing compound interest is vital to avoiding a debt trap that can become increasingly difficult to escape.

Difference Between Good Debt and Bad Debt

In the realm of personal finance, understanding the distinction between good debt and bad debt is crucial for sound financial planning. Good debt is typically characterized by loans that offer a potential return on investment and can enhance one’s financial position over time. Examples of good debt include student loans that fund higher education, which can lead to better job opportunities and increased earning potential.

On the other hand, bad debt generally refers to borrowing that does not improve one’s financial well-being and may even detract from it. This includes high-interest credit card debt incurred from purchasing non-essential items. Such debts often carry interest rates that significantly outpace any benefits the purchases might provide, leading to a drain on financial resources.

It’s important to manage and distinguish these debts effectively. While good debt can be a strategic tool to build wealth, bad debt should be minimized to avoid unnecessary financial strain and ensure long-term economic health.

How Late Payments Affect Your Financial Future

Late payments can severely impact your credit score, which is a critical factor in determining your financial health. Even a single missed payment can remain on your credit report for up to seven years, potentially affecting your ability to secure loans, mortgages, or even certain types of employment.

Accumulation of late payments may lead to higher interest rates as lenders perceive you as a high-risk borrower. This can make borrowing more expensive, leaving you with less disposable income and a reduced capacity to save for future needs.

Moreover, late fees and penalties often accompany delayed payments, adding unnecessary strain on your finances. Frequent late payments can snowball into a cycle of debt accumulation, making it difficult to achieve financial stability.

To safeguard your financial future, it is imperative to maintain a disciplined approach toward managing your bills. Setting up automated payments or reminders can help ensure that payments are made on time, thereby preserving your credit score and financial well-being. Prioritizing timely payments is a vital step toward a secure financial future.

Why Minimum Payments Aren’t Enough

When managing debt, many borrowers find themselves opting to pay only the minimum payments required each month. While this might seem like a convenient and affordable option in the short term, it is important to understand why relying solely on minimum payments can be a financially detrimental strategy.

The primary issue with minimum payments is that they are often just a small fraction of the total balance owed. This means the majority of your payment goes toward paying interest, with very little actually reducing the principal balance. As a result, it can take several years, if not decades, to completely pay off the debt, leading to higher overall interest costs.

Furthermore, making only minimum payments can have a negative impact on your credit score. A high outstanding balance relative to your credit limit can increase your credit utilization ratio, which might lower your credit score over time. This, in turn, affects your ability to obtain favorable rates on loans and other financial products in the future.

To effectively manage debt and limit the true cost over time, it’s essential to pay more than the minimum whenever possible. By doing so, you reduce the interest you’ll pay, shorten your payoff timeline, and improve your overall financial health.

Calculate Total Interest Paid Over Time

Understanding the true cost of debt necessitates a thorough evaluation of the interest payments that accrue over the life of a loan. Knowing how to calculate total interest paid is vital for anyone managing debt, as it provides a clearer picture of the financial implications involved.

Initially, the process involves identifying the principal amount, the annual interest rate, and the loan term. These elements are fundamental inputs in most interest calculation formulas. By employing the standard formula for simple interest, Interest = Principal × Rate × Time, borrowers can calculate the basic total interest.

However, many loans operate on a compound interest basis rather than simple interest. For compound interest, the calculation is more complex, utilizing the formula: A = P(1 + r/n)nt, where A represents the total amount including interest, P is the principal, r is the annual interest rate, n is the number of times interest is compounded per year, and t is the time the money is borrowed for.

Paying attention to these details is crucial as compound interest can significantly increase the total cost of borrowing, especially over longer periods. By understanding these calculations, borrowers can better strategize their repayment plans, knowing ahead of time exactly how much interest will accumulate over the life of the loan.

How Long-Term Debt Affects Credit Score

Long-term debt can have a substantial impact on a person’s credit score, which is a critical component of your overall financial health. When managed effectively, such debt can contribute to building a reliable credit history, showcasing your ability to make timely payments over extended periods. This can ultimately contribute to a higher credit score.

However, if repayment is mismanaged, long-term debt can become a financial burden that negatively affects your credit score. Missed or late payments are reported to credit bureaus, which can lead to a decrease in your score, presenting potential challenges for future credit applications.

Additionally, having high amounts of long-term debt relative to your available credit can impact your credit utilization ratio. This is a critical factor in credit scoring models. It’s advisable to maintain a balance between borrowed amounts and available credit to mitigate negative effects on your score.

In summary, while long-term debt can help build credit history, its management is key. Proactively handling debts and maintaining a low credit utilization ratio can protect and even enhance your credit score over time.

Create a Payoff Plan with Clear Milestones

Understanding the true cost of debt over time is crucial, and creating an effective payoff plan can significantly alleviate financial burdens. Establishing a strategy with clear milestones is essential to ensure progress and maintain motivation throughout your journey.

Start by assessing all your existing debts, including the interest rates and repayment terms. This evaluation will give you a clear picture of what you owe and what needs to be prioritized. List your debts from the highest interest rate to the lowest to determine which debts will need immediate attention.

Create a realistic budget that allocates a specific amount each month towards debt repayment. Ensure the budget considers your daily living expenses while earmarking a dedicated amount for debt payoff. Consistency with payments is key to seeing the plan through.

Set clear and achievable milestones. For instance, aim to pay off one credit card or loan within a set timeframe. Celebrate small victories as you reach each milestone, as this reinforces commitment and provides a sense of progress.

Periodically review and adjust your plan. Financial situations can change, and it’s important to adapt your plan accordingly to remain on track. Whether it means increasing your payment amounts or adjusting timelines, staying flexible ensures that your payoff plan remains effective.

In conclusion, a payoff plan with structured milestones not only helps in managing debt effectively but also fosters financial discipline, paving the way for a more secure financial future.

Monitor Your Debt Progress and Adjust

Effectively managing your debt requires consistent monitoring of your financial situation. Regularly reviewing your debts helps you understand your progress and make necessary adjustments to your repayment strategy.

Start by analyzing your monthly statements to track payments and interest rates. This practice not only keeps you informed about your current situation but also aids in recognizing any changes in your financial obligations.

When you notice fluctuations in your income or unexpected expenses, it’s crucial to reevaluate your plan. Consider options such as consolidating debts or refinancing to reduce interest rates and improve payment terms.

Staying proactive and adjusting your approach ensures you remain on the right path towards debt reduction, ultimately minimizing the long-term financial burden associated with borrowing.

{kind=link}