In today’s ever-evolving economic landscape, the significance of mastering personal financial management cannot be overstated. Whether you’re navigating student loans, planning a dream vacation, or aiming for early retirement, understanding the essential principles of saving money can make all the difference. Our article, “The 5 Golden Rules of Saving Money,” explores these crucial strategies and provides actionable insights to empower your financial future. By prioritizing responsible spending and smart saving, you can achieve both short-term and long-term financial goals with confidence. Join us as we delve into these pivotal rules, ensuring that you harness the knowledge to build a secure and sustainable financial foundation.

Always Pay Yourself First

A fundamental rule in the journey to financial stability is to always pay yourself first. This principle involves prioritizing savings by immediately setting aside a portion of your income before addressing any other expenses. By doing this, you ensure that saving becomes a non-negotiable part of your monthly budget.

When you pay yourself first, you are essentially treating your savings as your top priority. It’s advisable to automate this process by setting up transfers to a separate savings account on payday. This creates a steady habit of saving and minimizes the temptation to spend extra money.

Paying yourself first not only builds a solid foundation for long-term financial goals but also creates an emergency fund, providing a safety net during unforeseen circumstances. Embracing this rule ensures that your present expenses do not overshadow your future financial security.

Save Before You Spend, Not After

One of the most crucial principles of effective financial management is to prioritize saving before spending. This approach ensures that a portion of your income is allocated directly to your savings, rather than being an afterthought. By saving first, you establish a disciplined strategy that strengthens your financial future.

Automatically setting aside a portion of your paycheck can make this process seamless. This practice not only instills a sense of financial discipline but also helps in building a financial cushion, thereby safeguarding against potential financial uncertainties. The key is to treat savings as an essential expense, similar to housing or utilities, thus reinforcing the habit of saving consistently.

Adopting a ‘save before you spend’ mentality allows you to focus on living within your means. By making savings a priority, you inevitably limit impulsive expenditures and avoid falling into debt traps. This approach lays the foundation for financial security and enables you to plan effectively for long-term goals such as retirement or other substantial investments.

Treat Saving Like a Fixed Monthly Bill

One effective strategy to ensure consistent contributions to your savings is to treat saving like a fixed monthly bill. Just as you regularly pay your rent, mortgage, or utilities, you should allocate a specific amount of money to be deposited into your savings account every month.

By establishing a fixed savings amount, not only does this approach cultivate financial discipline, but it also eliminates the temptation to skip savings if money feels tight. This method ensures that you prioritize saving just as you would any other essential bill.

Additionally, automating this process can further strengthen this habit. Setting up automatic transfers from your checking account to your savings account can help you remain consistent and stress-free, as the money is tucked away before it can be spent impulsively.

Ultimately, adopting this strategy highlights the importance of consistency in building a financial cushion for future needs or emergencies. Over time, treating your savings with the same priority as your bills can lead to significant financial growth and security.

Don’t Rely on Willpower—Automate Your Savings

When it comes to saving money, relying solely on willpower can be a challenging endeavor. Life’s temptations and unexpected expenses often derail even the most disciplined saving plans. To ensure consistency and success, it is advisable to automate your savings.

Automatic savings eliminate the need for frequent decisions, which can easily lead to decision fatigue and ultimately to failure. By setting up an automatic transfer from your checking account to a designated savings account, you are committing to saving a certain amount of money at regular intervals. This method enhances financial discipline by removing the temptation to spend funds that are earmarked for savings.

Moreover, automating savings ensures that your savings grow steadily. This method allows you to benefit from compound interest over time, increasing your financial security. It is a simple yet effective strategy to reach your financial goals without having to rely on fleeting willpower.

Utilizing technology to establish a permanent, automated routine not only makes saving easier but also reduces stress. Trust in the automation process can free you from the worry of manual saving and provide a more disciplined approach to managing your finances.

Keep Emergency Savings and Investment Savings Separate

One of the fundamental principles of effective financial management is maintaining a clear distinction between your emergency savings and investment savings. Each serves a specific purpose and mixing them can jeopardize your financial stability.

Emergency savings are designed to provide a safety net that ensures you can cover unexpected expenses, such as medical emergencies or urgent repairs, without derailing your financial plan. It is best kept in a readily accessible account, allowing you to draw from it without delay.

In contrast, investment savings are meant for long-term growth. These funds are typically allocated into stocks, bonds, or other investment vehicles that may fluctuate in value over time. By keeping your investment savings separate, you allow them to grow according to your financial goals without the need to liquidate when unexpected expenses arise.

To ensure financial security, it is wise to maintain a dedicated account for each purpose. This separation not only aids in disciplined saving practices but also in strategic financial decision-making, which can lead to more robust economic well-being in the long run.

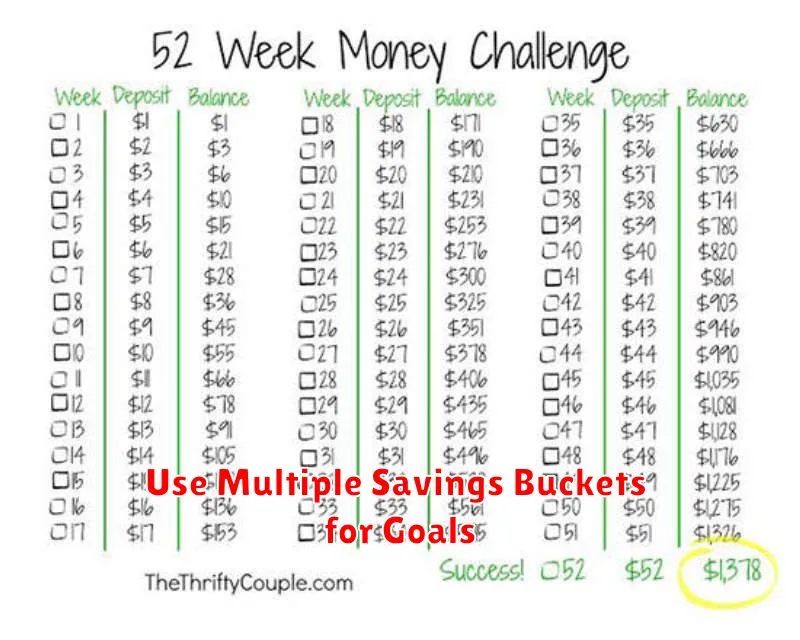

Use Multiple Savings Buckets for Goals

One of the most effective strategies to ensure you are successful in saving money is by using multiple savings buckets to earmark funds for different goals. By dividing your savings into distinct categories, you can manage your finances more efficiently and stay motivated.

Allocating resources to separate accounts specifically designated for each goal can help in tracking your progress effectively. For instance, consider creating buckets for emergency funds, vacations, education, and retirement. This not only clarifies your financial intentions but also prevents the unintended use of funds for other purposes.

Furthermore, utilizing multiple buckets can provide a psychological advantage. Seeing each bucket grow as you deposit funds can be significantly rewarding, acting as a strong motivator to continue saving diligently. This approach encourages financial discipline while offering the flexibility to prioritize certain goals when necessary.

In conclusion, adopting the practice of using multiple savings buckets is a smart strategy to achieve financial success. It helps ensure that each of your aspirations gets the dedicated attention it deserves, fostering a sense of security and accomplishment as you work towards each goal.

Track and Celebrate Savings Milestones

Tracking your savings progress is a vital strategy in effectively managing personal finances. By setting clear and realistic savings goals, you establish a tangible benchmark to measure your progress. Regularly reviewing your savings allows you to remain focused and motivated on your financial journey.

While setting milestones may seem trivial, each milestone represents a significant achievement. These milestones help in breaking down your overall savings target into more manageable portions. For example, if you’re saving for a $10,000 emergency fund, celebrating when you reach $1,000, $5,000, and so forth can boost your morale and encourage continued savings.

Celebrating these achievements is equally important. Taking time to acknowledge your progress reinforces positive behavior and sustains motivation. While these celebrations need not be extravagant, simple acknowledgments such as a small treat or a day off can serve as powerful reminders of your financial discipline and commitment.

Ultimately, tracking and celebrating savings milestones not only enhances financial discipline but also transforms saving from a mundane task into an engaging and emotionally rewarding journey towards financial security and independence. It’s an essential component of any successful savings plan.

Keep Your Lifestyle Below Your Income

One of the most fundamental principles of financial stability is ensuring that your lifestyle remains below your income. By adhering to this principle, you can cultivate a savings habit that protects against unexpected expenses and enhances your financial security.

Spending less than you earn allows for the creation of a buffer that can be allocated towards savings and investments. This approach not only ensures that you live within your means but also prepares you for potential financial opportunities.

It’s crucial to evaluate your spending habits regularly. Prioritize your needs over your wants and minimize discretionary expenses. This strategy not only reinforces financial discipline but also prevents potential debt accumulation.

Living below your means does not imply a reduction in life quality but promotes a mindful approach to financial decisions, ensuring long-term monetary health and peace of mind.

Review Your Savings Plan Quarterly

To achieve your financial goals, it’s crucial to review your savings plan quarterly. This practice helps you stay on track, making adjustments as necessary and ensuring that you are capitalizing on any opportunities for improvement.

Your financial situation can change rapidly, whether it’s due to changes in income, expenses, or other personal circumstances. By revisiting your savings strategy every three months, you can adapt accordingly, ensuring your plan remains aligned with your current reality.

Moreover, regular reviews allow you to celebrate milestones, reinforcing positive saving habits. It also provides a chance to reassess your goals, making sure they are still realistic and relevant. This consistent evaluation ensures that your savings plan remains effective and dynamic.

During your review, pay attention to key details such as interest rates, investment returns, and any policy changes that might impact your savings. By staying informed and proactive, you maintain control over your financial journey, optimizing your path towards achieving your financial aspirations.

{kind=link}