In today’s rapidly evolving financial landscape, mastering the art of money management has become more crucial than ever. Whether you’re looking to enhance your savings, reduce debt, or optimize your spending, understanding how to effectively manage your finances can lead to a healthier financial future. This guide, “10 Smart Ways to Manage Your Money Better,” offers practical insights and strategies to help you take control of your financial destiny. Delve into the world of budgeting, investment, and spending as we explore the smartest ways to secure your financial well-being and achieve ultimate financial stability.

Track Every Dollar You Spend

Tracking every dollar you spend is a crucial step in managing your finances effectively. By keeping a detailed account of your spending, you can identify unnecessary expenses and allocate funds more efficiently. This practice encourages financial awareness, helping you see exactly where your money goes and where you might need to cut back.

To start, consider utilizing budgeting apps or financial software that align with your needs. These tools can provide real-time updates on your expenditures, making it easier to stay on top of your budget. They also often offer features like expense categorization and spending reports, which can offer insights into your habits and guide better decision-making.

Additionally, maintaining a simple spreadsheet can be a highly effective method for those who prefer a more hands-on approach. List all your expenditures and incomes to maintain transparency in your financial activities. Reviewing this data regularly can lead to more informed decisions about saving, investing, and spending.

Ultimately, being consistent with tracking your spending will lead to better financial management and, potentially, greater savings. This practice not only aids in avoiding overspending but also provides peace of mind by cultivating a mindful approach to managing money.

Create a Realistic Monthly Budget

Creating a realistic monthly budget is a fundamental step towards effective financial management. Start by thoroughly evaluating your monthly income sources, ensuring you account for all potential earnings. Once you have a clear picture of your earnings, categorize your expenses into fixed and variable types. Fixed expenses, such as rent or mortgage payments, are consistent each month, whereas variable expenses like groceries and entertainment can fluctuate.

When setting your budget, ensure you allocate a portion of your income towards savings and emergency funds. It’s crucial to strike a balance between saving for the future and covering immediate needs. Aim for a savings target that complements your financial goals, whether it’s buying a home, planning a vacation, or preparing for retirement.

Throughout the month, track your spending to ensure you stay within your budget limits. Use budgeting tools or apps that can send alerts when nearing your spending thresholds. Maintain flexibility by adjusting categories if you find you’ve underestimated your needs in one area and overestimated in another. Regularly review your budget to align with any changes in income or life circumstances.

By implementing these strategies, you can develop a realistic budget that not only guides your monthly spending but also sets a strong foundation for long-term financial health.

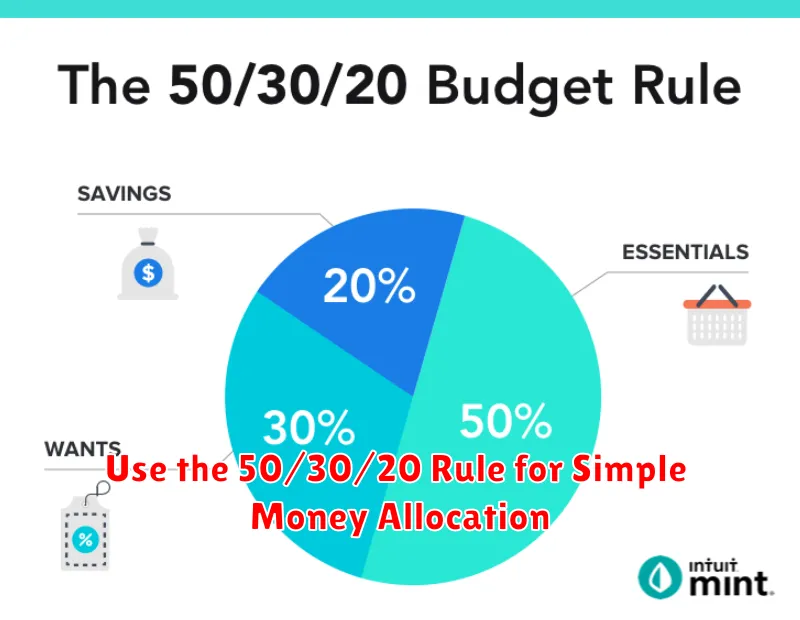

Use the 50/30/20 Rule for Simple Money Allocation

One effective method to manage your finances wisely is the 50/30/20 rule, a straightforward strategy for budgeting and saving. This rule provides a simple framework for allocating your income into three main categories: needs, wants, and savings.

According to the 50/30/20 rule, allocate 50% of your income to essential expenses, such as housing, utilities, groceries, and transportation. These are necessities you cannot do without. By limiting this to half of your income, you ensure that you are not overspending beyond your means on obligations.

Next, dedicate 30% of your income to discretionary spending, the “wants.” This could include dining out, entertainment, vacations, and other non-essential activities. It allows you the flexibility for leisure and fun while keeping spending in check.

The final 20% should be directed towards savings and debt repayment. This includes contributions to your retirement fund, emergency savings, and paying down any debts you owe. Prioritizing this segment ensures you are preparing for the future and reducing financial strain from interest-bearing liabilities.

By implementing the 50/30/20 rule, you can maintain a balanced budget that supports both your current lifestyle and future financial health. It eliminates the guesswork and provides clarity, leading to more informed financial decisions.

Set Financial Goals for Short and Long Term

Setting financial goals is essential for achieving financial stability and success. By differentiating between short-term and long-term goals, you can create a structured plan to manage your money effectively.

Short-term goals typically focus on objectives you aim to achieve within a year or two. These might include creating an emergency fund, paying off small debts, or saving for a vacation. Establishing these goals can provide immediate satisfaction and build a foundation for future financial endeavors.

On the other hand, long-term goals usually span over several years and require strategic planning and patience. Savings for retirement, buying a home, or investing in your child’s education are examples of such goals. Establishing these helps you stay committed to larger life ambitions, offering motivation and direction for your financial plans.

To effectively set these goals, start by being specific about what you want to achieve and assign a timeline and dollar amount to each goal. Regularly review and adjust your goals based on changes in your life circumstances, and consider enlisting the help of financial advisors if necessary. These strategic steps ensure you stay on track to attain both immediate and future financial success.

Avoid Impulse Purchases by Using a 24-Hour Rule

Impulse buying can significantly disrupt your financial health, often leading to unnecessary expenses and regret. One effective strategy to prevent this is implementing the 24-hour rule. By adopting this approach, you give yourself a mandatory 24-hour period to consider any non-essential purchase.

The intention behind the 24-hour rule is to allow time for rational decision-making, rather than succumbing to spontaneous urges. During this period, reflect on whether the item is a necessity or if it aligns with your financial goals. This pause helps in distinguishing between a genuine need and a fleeting want.

By exercising patience and practicing this rule, individuals often find that their desire for the item diminishes, leading to a more thoughtful spending habit. Consistently applying the 24-hour rule fosters better financial discipline, promoting savings and reducing clutter from unnecessary items. It’s a simple, yet powerful method to manage your finances effectively by curbing impulsive spending.

Review and Adjust Your Budget Regularly

One of the most essential practices in effective money management is to periodically review and adjust your budget. This allows you to reflect changes in your financial situation and ensure you’re on track with your financial goals.

A monthly review is ideal to assess your income and expenses, identify unnecessary spending, and allocate funds to more crucial areas. Regularly updating your budget helps you accommodate for unexpected expenses, adjust for salary changes, or align with new priorities.

It is crucial to remain flexible yet disciplined. Understand that a budget is dynamic; it can and should be adjusted as your life circumstances evolve. By staying proactive, you can avoid financial pitfalls and seize opportunities to enhance your financial well-being.

Use Automation to Pay Bills and Save

In today’s digital era, leveraging automation to handle your financial responsibilities is a prudent strategy for managing money effectively. Automated bill payments ensure that you meet your financial obligations promptly, preventing late fees and maintaining a strong credit score. By scheduling monthly payments through your bank or financial service platforms, you can eliminate the stress of manual bill handling.

Aside from managing bills, automation can be a powerful tool to boost your savings. Consider setting up automatic transfers from your checking to savings accounts. This method promotes consistent saving habits and helps you build a financial cushion over time. Reallocating funds automatically can also offer peace of mind, as regular transfers are made without requiring your constant attention.

By integrating automation into your financial practices, you simplify your financial management and pave the way for achieving larger financial goals. It’s a smart, effortless approach that ensures you prioritize both payments and savings, ultimately enhancing your financial health.

Choose the Right Bank and Accounts for Your Needs

Selecting the right bank and accounts is essential for managing your finances effectively. When choosing a bank, consider factors such as convenience, fees, and the range of services offered. Ensure the bank provides easy access through online and mobile banking platforms, as well as physical branches if needed.

Examine the types of accounts available, such as checking, savings, and investment accounts. Opt for those that align with your financial goals. For example, if you aim to save money, a high-yield savings account may be beneficial. Compare the interest rates and potential fees associated with each account type.

Additionally, consider the bank’s customer service standards and security measures. Strong customer support can be crucial in resolving issues quickly, while robust security ensures the protection of your financial information.

By carefully evaluating your banking options, you can choose a bank and accounts that cater to your specific needs, ultimately enhancing your financial management strategy.

Understand Where You Can Cut Costs

In today’s economic climate, being mindful of your spending is crucial. To better manage your finances, it’s important to identify areas where you can cut costs without compromising your quality of life.

Begin by analyzing your current expenses. Categorize them into essentials such as housing and groceries, and non-essentials such as dining out or entertainment. For non-essential spending, consider setting limits or exploring cheaper alternatives.

A smart approach to reducing costs is to renegotiate bills or subscriptions. Contact service providers to see if there are any discounts or deals that could lower your monthly expenses.

Furthermore, keep track of small expenses, which often add up unnoticed. Creating a detailed budget will help you stay on top of your spending habits and identify areas ripe for savings.

By continually monitoring and adjusting your expenses, you can effectively cut costs and free up funds for more critical needs or savings priorities.

Build a Habit of Monthly Financial Review

Developing a routine to conduct a monthly financial review is a pivotal step towards achieving financial stability. Regularly evaluating your finances ensures that you stay on track with your financial goals and helps you make informed decisions. By understanding where your money is being allocated, you can identify areas of improvement and adjust your spending habits accordingly.

Start by setting a fixed date each month to review your financial statements. This includes your bank account, credit card bills, and any investment portfolios. Tracking these regularly instills awareness and discipline, allowing you to pinpoint any discrepancies early on.

During your review, categorize your expenses into essential and non-essential. This distinction highlights opportunities to cut back on unnecessary spending and allocate funds towards more beneficial avenues like savings or investments.

In addition, a monthly review allows you to reassess your budget and financial goals, ensuring they align with your current financial situation and aspirations. Whether it’s increasing your savings rate, paying off debt, or planning for a big purchase, regular reviews provide the opportunity to recalibrate your path to success.

Lastly, incorporating technology can further enhance this practice. Utilize financial management tools or apps to automate part of the process, such as tracking transactions and setting reminders for bills. This not only saves time but also ensures a more accurate financial overview.

Building the habit of reviewing your finances monthly ensures that you remain proactive about managing your money, paving the way for financial health and long-term success.

{kind=link}